From The Daily Capitalist

Interesting things have been happening in the real estate markets.

Residential

The home sales index spike from the home buyer tax credit has almost run out. If you didn't have a deal in escrow by April 30, you didn't get the credit. The time to close a deal was extended to September 30. The predictions were that we'd see a fall in July activity which is exactly what is occurring.

The reports that are currently coming in don't yet reflect July sales which will show a drop in sales. For example, the Case-Shiller report came in yesterday for May, 2010, but that report is a three-month average of prices. The report said prices were up 1.2% MoM, and 5.4% YoY. That was the peak of housing credit driven sales. According to S&Pwhich publishes the index:

"While May's report on its own looks somewhat positive, a broader look at home price levels over the past year" doesn't show that the housing market "is in any form of sustained recovery," said David M. Blitzer, chairman of S&P's index committee. "Since reaching its recent trough in April 2009, the housing market has really only stabilized at this lower level."

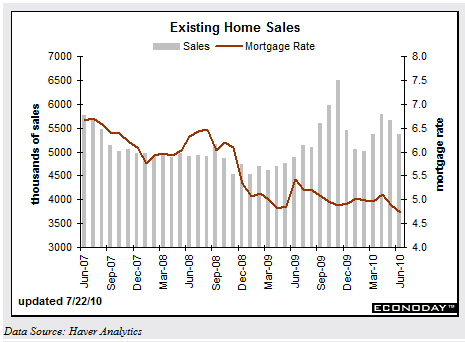

Last week the National Association of Realtors reported that June sales of existing homes declined 5.1% from May but up 9.8% YoY. Sales declined 9.3% in the west. Inventory rose in June:

The supply of homes available for sale in 27 major metropolitan areas at the end of June was up 3.7% from one month earlier, according to figures compiled by ZipRealty Inc., a real-estate brokerage firm based in Emeryville, Calif.

Ivy Zelman of Zelman Associates says for the past 27 years inventories have declined in June by 0.5%.

I showed this chart last week (click to enlarge):

Monday the FHA reported that the level of its insured mortgages more than 90 days overdue or in foreclosure jumped 35% YoY. But:

According to the FHA June single-family operations report, the total volume of mortgage in-force increased more than 24% to 6.4m in June compared to the same month one year ago. The total value of unpaid FHA mortgages was $865.5bn in June, up 30.3% from $663.8bn one year ago and up 3.3% from $837.8bn in May. ... But with that increase came a rise in serious delinquencies, 7.6% last year, compared to 8.3% in June. ...Based on applications received, the FHA said the seasonally adjusted annual rate of applications was nearly 1.9m, down 13% from the previous month's rate and the lowest since January's rate of 1.69m.

What this means is that most home loans are being financed with government guarantees from the FHA, Freddie (FMCC.OB) and Fannie (FNMA). I had thought the FHA had run out of money, but apparently their limits have been extended. The last numbers I saw said that 90% of loans are government backed.

According to Bloomberg yesterday, in an article about a surge in people renting apartments:

Finances for homeowners didn’t improve fast enough to prevent more than 1.65 million foreclosure filings in the first half, an increase of 8 percent from the same period in 2009, RealtyTrac Inc., a data company in Irvine, California, said July 15. A record 269,962 U.S. homes were seized from delinquent owners in the second quarter as lenders set a pace to claim more than 1 million properties by the end of 2010.

But here is probably the most significant statistic: home ownership rates have fallen to 66.9 from a high of 69.2% in 2004. In my Megatrendsarticle, I expected this to happen as home ownership rates revert to the statistical historic averages. This does not bode well for housing prices unless we see substantial increase in either population or inflation.

The sad fact is that the first time home buyer credit has substantially distorted the housing market and has hampered recovery. One could say that such meddling has set back recovery for nine months, or since last Fall when the tax credit began to artificially stimulate sales. Home prices will now stay under pressure as foreclosures continue to rise which will cause inventory to rise.

Commercial

Last week Fitch reported that defaults of commercial real estate backed mortgages (CMBS -- the CRE equivalent of residential mortgage backed securities) are increasing. They pointed to 8 properties held in CMBS portfolios are likely to default in August, each more than $20 million. They are interest only loans that were refinanced five years ago and now cannot get the financing to take out their existing lenders.

In August, Fitch expects 115 loans worth $1.3bn in balances to fall into special servicing and more to come through the rest of 2010, peaking in October at 181 loans at $2.1bn and totaling more than 772 loans worth $7.8bn. ...With more commercial mortgage-backed securities (CMBS) loans on the verge of default this Fall, special servicers are being forced to accelerate them through the REO process to avoid building a shadow inventory similar to the one in residential.

Also Deutsche Bank reported:

... that the number of new transfers into special servicing will continue to outpace commercial loan workouts. But once properties are ready for liquidation, valuations on commercial real estate are missing the mark, according to Deutsche Bank. ...The analysts projected an 18% delinquency rate on CMBS. Since the beginning of 2010, the balance of loans at least 90-days delinquent has increased every single month.“The implications for special servicers are potentially dire,” according to the Deutsche Bank report. “If they wait too long to foreclose or restructure loans, the number of loans in their portfolios will continue to build, so even when they finally resolve an asset it might not even make a dent.”

Based on my own anecdotal evidence and a review of earnings reports of regional and local banks, it appears that lenders are starting to deal with bad CRE loans rather than just "extend and pretend":

Many community and regional banks have aggressively charged off loans, mostly in commercial and construction financing. Despite signs of stability in delinquencies, banks still have to reappraise properties that serve as collateral. And when appraisals come in lower, the bank has to write it down, whether or not the loan is delinquent which in turn, hurts capital.

Wells Fargo (WFC) in its recent earnings release said:

Losses in the commercial portfolio continued to improve from the higher levels experienced last year, including a 10 percent linked quarter reduction in commercial real estate losses.

Reports from people I know who are active in CRE in the L.A. area also lead me to believe that lenders are starting to do deals on REO properties. While two years ago no deals were being made, today there is more opportunity and activity. Further there appears to be less "extend and pretend" as banks are less willing to accommodate defaulting borrowers; lending standards have tightened rather than loosened. They have about $500 billion in CRE loans maturing in the next couple years.

In my view, it is CRE that is critical to a recovery. We will need to see more positive signs, such as an increase in business loans, more CRE foreclosures, and a reduction in bank excess reserves, before we can say there is some kind of trend, but it could be that the CRE logjam is starting to break up. I do not expect any recovery of the CRE market any time soon because of the volume of debt maturing, but I am beginning to think that more defaults will be pushed into special servicing resulting in foreclosures. The result will be further downward pressure on CRE prices (they have already declined 24% since the peak in Fall 2007).

No comments:

Post a Comment

Comment on this article